Municipals were a tad firmer ahead of the Fourth of July holiday, as U.S. Treasury yields fell and equities ended mixed.

The Federal Open Market Committee meeting minutes released after the early market close signaled the Fed is in no hurry to cut rates.

FOMC members saw inflation “diminishing” but still needed more evidence it was heading toward their 2% target before lowering interest rates, although several officials would consider a rate hike if inflation not moderate further, according to minutes of the June 11-12 meeting.

“Participants noted that progress in reducing inflation had been slower this year than they had expected last December,” according to the minutes. “They emphasized that they did not expect that it would be appropriate to lower the target range for the federal funds rate until additional information had emerged to give them greater confidence that inflation was moving sustainably toward the Committee’s 2% objective.”

Officials noted the importance of remaining data-dependent. “Several participants noted that financial market reactions to data and feedback received from contacts suggested that the Committee’s policy approach was generally well understood,” the minutes said.

“There is still uncertainty about the economic outlook and until that uncertainty clears there is no consensus on the committee to begin rate cuts,” said Brian Rehling, head of Global Fixed Income Strategy at Wells Fargo Investment Institute. “We remain in wait and see mode — upcoming data, especially jobs and inflation are key.”

Scott Anderson, chief U.S. economist and managing director at BMO Economics, said he still expects the rate cuts to begin in September. The Fed ” is clearly on hold,” while data “is gradually moving in the right direction.”

Triple-A yields fell one to three basis points while Treasuries were better by four to eight.

The two-year muni-to-Treasury ratio Wednesday was at 66%, the three-year at 66%, the five-year at 67%, the 10-year at 66% and the 30-year at 83%, according to Refinitiv Municipal Market Data’s 1 p.m. EST read. ICE Data Services had the two-year at 65%, the three-year at 66%, the five-year at 66%, the 10-year at 66% and the 30-year at 81% at 1 p.m.

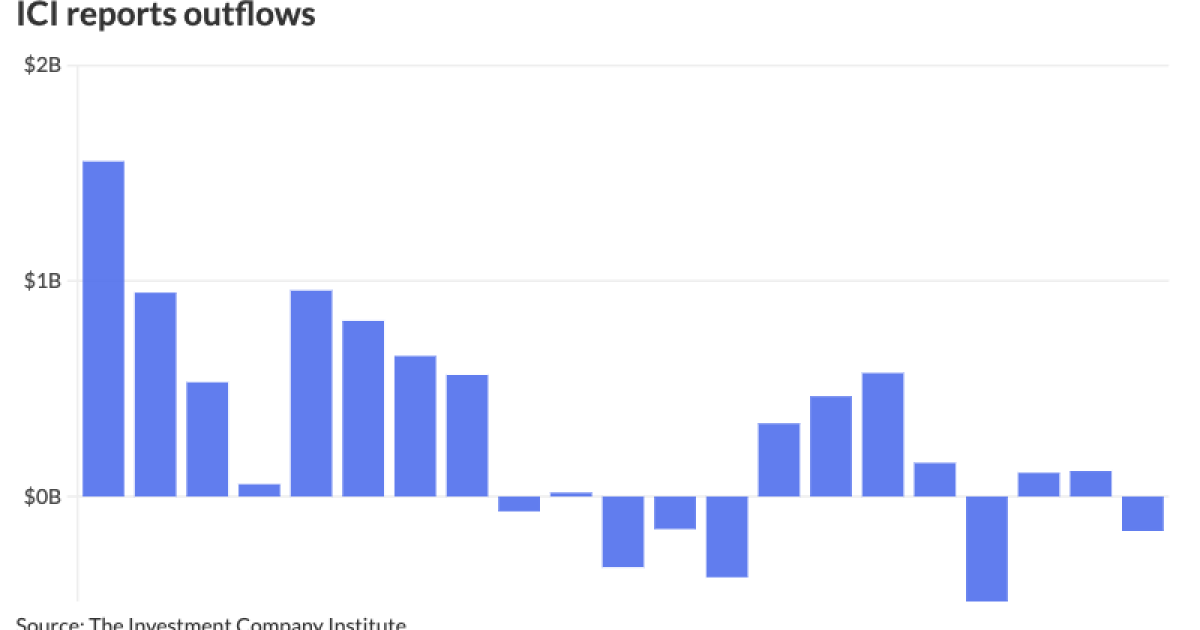

The Investment Company Institute reported Wednesday $160 million of outflows into municipal bond mutual funds for the week ending June 26 following $118 million of inflows the week prior.

Exchange-traded funds saw outflows at $411 million, following inflows of $220 million the week prior.

“The forces of municipal fundamental and technical measures are setting up a reconciliation against higher UST yields,” said Kim Olsan, senior vice president of municipal bond trading at FHN Financial.

July is in the middle of the

The Federal Open Market Committee will meet in mid-July and “issuers will be mindful of November’s election and likely pre-fund transactions through the summer to capture larger rollover needs,” Olsan said.

Five- and 10-year tenors are higher than the last 12 months’ average ranges, she said.

In the five-year area, high-grade munis “are trading just through 3.00%, or about 20 basis points above their annual median, she noted.

“Intermediate AAA bonds have settled around 2.90%, nearly 15 basis points higher than the annual median,” while “long-dated bonds near 3.75% (for pure AAA specialty state names) are within a nominal spread to a 3.80% average since July 2023,” Olsan said.

Many AA-rated revenue bonds can be bought at 4.00% or better, and carry taxable equivalent yields over 6.00%, she said.

As an example, a recent issue of Massachusetts Bay Area Transportation sales tax bonds saw 5s due 2048, callable in 2034, at 3.95%, Olsan said.

Above-average value can be seen in yields along most of the curve, she said.

Supply could start to take on a “larger bifurcated nature,” according to Olsan.

“There is some likelihood that heavier volume in general market names could create spread widening while substantial supply deficits in high-tax states (CA, NY, MA, NJ, MD) could begin to compress spreads,” she said, pointing to recent trades that show a “potential pattern.”

Los Angeles Department of Water and Power 5s due 2037 (call 2034) “traded at 3.00% and flat to the MMD spot but University of Texas 5s due 2035 (call 2034) were sold at 3.10% for a spread of +20/MMD,” she said.

Over the past several years, July seasonality has been “heavily directed” by supply and pre- and post-tightening cycle forces, Olsan said.

“High demand/low yield periods” were seen in 2020 and 2021, she said.

The first week of July in 2020 saw the 10-year yield end at 0.90% before rallying through month end to close at 0.65%, Olsan said.

July 2020 saw $47 billion of new issuance, where the “demand fed larger supply,” she said.

Similarly, July 2021 saw the 10-year yield fall from 0.98% to 0.82% on $37 billion in issuance, Olsan said.

However, July 2022 and 2023 saw “mismatched results,” Olsan said.

The effect of the fourth Fed rate hike in 2022 impacted July supply, which saw $28 billion of issuance, Olsan said.

Reinvestment demand moved the 10-year yield from 2.66% to 2.21% through the end of July 2022, she said.

Meanwhile, “a modest 25 basis point rate hike had a muted effect on both yield direction and supply (just $27 billion was priced),” in July 2023, she said.

The 10-year MMD yield in 2023 was at 2.56% at the start of the month before selling off ”marginally” mid-month and finishing nearly flat, Olsan said.

“Any surge this month in general-market volume could produce a higher yield set across most sectors,” she said.

Despite issuance falling to a paltry $245 million this week, there are already several large deals on the horizon. Bond Buyer 30-day visible supply grows to $11.93 billion.

The Dormitory Authority of the State of New York is set to sell July 10 $1.29 billion of state sales tax revenue bonds in three series.

Harris County is set to price next week a $730 million deal, consisting of $100 million of permanent improvement refunding bonds, $220 million of unlimited tax road refunding bonds and $410 million of permanent improvement tax and revenue certificates of obligation.

The Washington Metropolitan Area Transit Authority is set to price July 9 $625 million of second lien dedicated revenue bonds.

The New York City Transitional Finance Authority is set to price the week of July 15 $1.7 billion of tax-exempt and taxable future tax-secured revenue refunding bonds.

Miami-Dade County, Florida, is set to price July 16 $923 million of aviation revenue refunding bonds, consisting of $782 million of AMT bonds and $141 million of non-AMT bonds.

New York City is set to price the week of July 29 $1.2 billion of GO refunding bonds.

The Port of Seattle is set to price the week of July 29 around $850 million of AMT and non-AMT intermediate lien revenue and refunding bonds.

Houston is set to price a $720.445 million deal, consisting of $589.41 million of GO refunding bonds and $131.035 million of public improvement refunding bonds.

AAA scales

Refinitiv MMD’s scale saw bumps five years and in: The one-year was at 3.12% (-3) and 3.08% (-2) in two years. The five-year was at 2.90% (-2), the 10-year at 2.87% (unch) and the 30-year at 3.75% (unch) at 1 p.m.

The ICE AAA yield curve was bumped three basis points: 3.19% (-3) in 2025 and 3.12% (-3) in 2026. The five-year was at 2.92% (-3), the 10-year was at 2.89% (-3) and the 30-year was at 3.72% (-3) at 1:30 p.m.

Bloomberg BVAL was bumped up to one basis point: 3.17% (-1) in 2025 and 3.12% (-1) in 2026. The five-year at 2.95% (-1), the 10-year at 2.86% (-1) and the 30-year at 3.76% (-1) at 1:30 p.m.

Treasuries were firmer.

The two-year UST was yielding 4.703% (-4), the three-year was at 4.488% (-6), the five-year at 4.319% (-7), the 10-year at 4.353% (-8), the 20-year at 4.629% (-8) and the 30-year at 4.523% (-8) at 1:45 p.m.

Gary Siegel contributed to this report.