Municipals were little changed Tuesday as most investors were awaiting new-issue supply, U.S. Treasuries offered little direction in a mixed session and equities were down near the close.

Wednesday will see the release of January’s Federal Open Market Committee Meeting minutes, which “should show any division amongst the committee members as to the continued direction of the current rate cycle,” said Jay Woods, chief global strategist at Freedom Capital Markets.

While the market “rarely moves dramatically on the minutes, this may set the tone for the FOMC’s upcoming March meeting,” he noted.

Market participants agree the Fed will not cut rates in March, but the focus now moves to the May meeting, with the odds of a cut at that time having shifted, Woods said.

The probability of a May rate cut was at 60% over a month ago, but after last week’s hotter-than-expected inflationary data, odds have fallen to under 35%, he said.

While the

Munis are down negative 0.20% month-to-date, bringing year-to-date returns to negative 0.71%, according to Bloomberg data.

While muni yields were little changed Tuesday, rising up to two basis points, depending on the scale, yields have risen an average of 18 basis points in February and 26 basis points since the beginning of the year, Wong said.

“With the new economic data signaling a delay of the Fed starting rate cuts to further into the year, we should continue to see yields rise until we get near to the Fed’s target of a 2% ‘neutral’ rate for inflation,” he said.

“The muni market outperformed the rate weakness [last] week in a sign that there is still plenty of cash on the sidelines, while the primary calendar has been underwhelming,” Birch Creek Capital strategists said in a weekly report.

Investors pulled money from muni mutual funds for the second consecutive week, with LSEG Lipper reporting $142 million of outflows after $121 million the week prior.

The outflows from muni mutual came from exchange-traded funds, which saw $471 million of outflows, versus $329 million of inflows from ex-ETFs.

The buyer base has remained “patient” even as muni-UST ratios are rich, with “many funds on the sidelines waiting to pounce on any weakness,” they said.

The two-year muni-to-Treasury ratio Tuesday was at 60%, the three-year at 59%, the five-year at 58%, the 10-year at 58% and the 30-year at 81%, according to Refinitiv Municipal Market Data’s 3 p.m. EST read. ICE Data Services had the two-year at 60%, the three-year at 58%, the five-year at 58%, the 10-year at 58% and the 30-year at 80% at 3:30 p.m.

It is expected if there is a period of UST stability or strength, the muni market “would likely gap higher as this cash comes rushing into the market,” Birch Creek strategists said.

This dynamic, they noted, has led to a “relatively calm trading environment.”

Customer purchases came in near recent averages, mainly driven by separately managed account buyers in the five- to 20-year range, they noted.

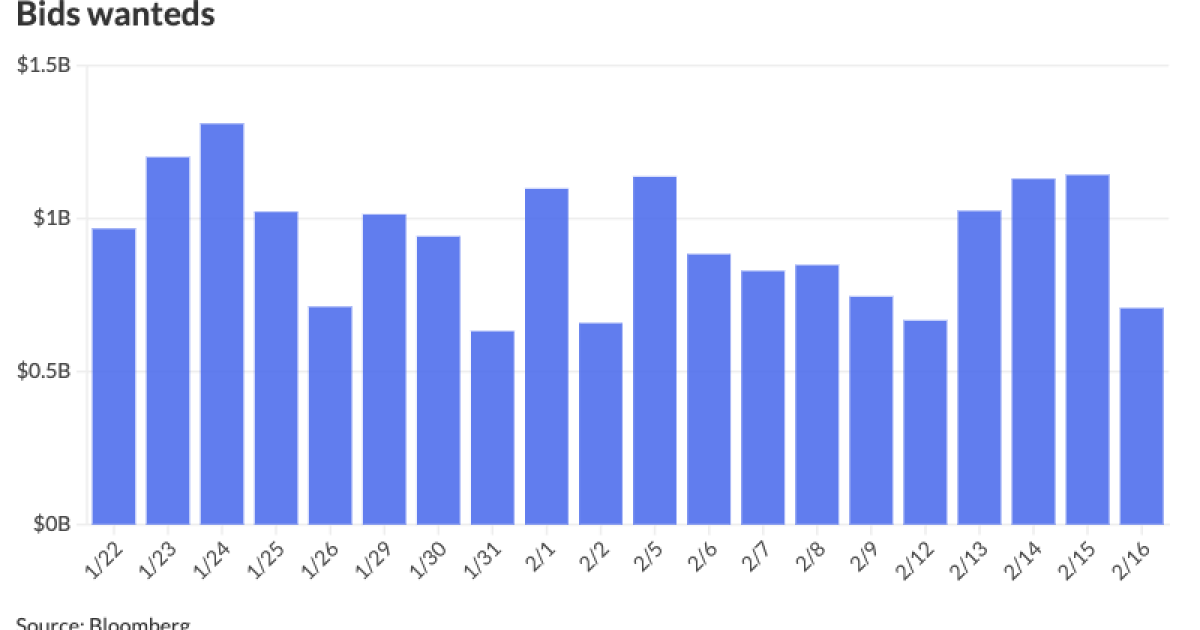

On the other hand, bid wanteds “were a little below average, with a large chunk coming from ETFs,” they said.

Investors put up around $4.67 billion up for the bid with Thursday seeing the large volume of bids-wanted at $1.14 billion, according to Bloomberg.

“With supply continuing to be low, we should start to see secondary trading volume pick up as investors continue to put their money to work,” Wong said.

March and April are usually “weaker months for munis as the technical picture reverses, so unless fund flows can overwhelm the pickup in supply, there are likely better opportunities ahead,” Birch Creek strategists said.

Secondary trading

Maryland 5s of 2025 at 2.85% versus 2.89% Wednesday and 2.89% on 2/7. Virginia College Building Authority 5s of 2026 at 2.78% versus 2.76% Thursday and 2.78% Wednesday. California 5s of 2027 at 2.53% versus 2.49% Friday and 2.54% Thursday.

North Carolina 5s of 2028 at 2.51% versus 2.46% Thursday. Washington Suburban Sanitary Commission 5s of 2029 at 2.48%. NYC 5s of 2030 at 2.55%-2.54%.

Massachusetts Clean Water Trust 5s of 2033 at 2.39%. Florida BOE 5s of 2034 at 2.48% versus 2.49% Thursday and 2.42%-2.39% on 2/1. Wisconsin 5s of 2035 at 2.67%.

East Bay Utility District waters, California, 5s of 2049 at 3.46%-3.45% versus 3.44%-3.45% Friday and 3.54% original on Thursday. Massachusetts 5s of 2052 at 3.82% versus 3.86% Thursday and 3.83%-3.78% on 2/13.

AAA scales

Refinitiv MMD’s scale was unchanged: The one-year was at 2.96% and 2.76% in two years. The five-year was at 2.46%, the 10-year at 2.46% and the 30-year at 3.59% at 3 p.m.

The ICE AAA yield curve was little changed basis point: 2.97% (unch) in 2025 and 2.78% (+1) in 2026. The five-year was at 2.48% (unch), the 10-year was at 2.49% (unch) and the 30-year was at 3.55% (-1) at 3:30 p.m.

The S&P Global Market Intelligence municipal curve was cut up to two basis points: The one-year was at 2.96% (+2) in 2025 and 2.76% (+2) in 2026. The five-year was at 2.46% (+2), the 10-year was at 2.47% (unch) and the 30-year yield was at 3.57% (unch), according to a 3 p.m. read.

Bloomberg BVAL was unchanged: 2.96% in 2025 and 2.81% in 2026. The five-year at 2.46%, the 10-year at 2.53% and the 30-year at 3.65% at 3:30 p.m.

Treasuries were firmer 10 years and in.

The two-year UST was yielding 4.607% (-4), the three-year was at 4.383% (-3), the five-year at 4.246% (-3), the 10-year at 4.270% (-1), the 20-year at 4.560% (flat) and the 30-year at 4.442% (+1) at 3:45 p.m.

Negotiated calendar

The New Jersey Educational Facilities Authority (Aaa/AAA//) is set to price Wednesday $659.060 million of Princeton University revenue bonds, consisting of $500 million of new-issue bonds, 2024 Series B, and $159.060 million of refunding bonds, 2024 Series C. Goldman Sachs.

The Maryland Transportation Authority (Aa2//AA/) is set to price Thursday $628.325 million of tax-exempt transportation facilities projects revenue refunding bonds, Series 2024A. BofA Securities.

The Michigan State Housing Development Authority (Aa2/AA+//) is set to price Thursday $424.675 million of social single-family mortgage revenue bonds, consisting of $248.350 million of non-AMT bonds, 2024 Series A, serials 2024-2036, terms 2039, 2044, 2049, 2053, 2054; $126.325 million of taxables, serials 2024-2034, terms 2039, 2044, 2050; and $50 million of taxable variable rate bonds, 2024 Series C, term 2054. Barclays Capital.

The Regents of the Board of the University of Texas System (Aaa/AAA/AAA/) is set to price Wednesday $375 million of Permanent University Fund bonds, Series 2024A. Wells Fargo.

The California Infrastructure and Economic Development Bank (A2///) is set to price Thursday $281.450 million of California Academy of Sciences sustainability revenue bonds, consisting $140.725 million of Series 2024A and $140.725 million of Series 2024B. Wells Fargo.

The Connecticut Housing Finance Authority (Aaa/AAA//) is set to price Wednesday $196.885 million of social Housing Mortgage Finance Program bonds, 2024 Series A, serials 2024-2036, terms 2039, 2044, 2049, 2051, 2054. BofA Securities.

The Virginia Housing Development Authority (Aa1/AA+//) is set to price Thursday $177.070 million of non-AMT rental housing bonds, 2024 Series A, serials 2026-2036, terms 2039, 2044, 2049, 2054, 2059, 2065. BofA Securities.

The Wisconsin Health and Educational Facilities Authority (Baa2///) is set to price Wednesday $163.720 million of Forensic Science and Protective Medicine Collaboration Project revenue bonds, Series 2024, serial 2027. Raymond James.

The Creek County Educational Facilities Authority, Oklahoma, (/AA//) is set to price Thursday $153.840 million of BAM-insured Sapulpa Public Schools Project educational facilities lease revenue bonds, Series 2024. D.A. Davidson.

The North Dakota Housing Finance Agency (Aa1///) is set to price Wednesday $149 million of social non-AMT Home Mortgage Finance Program housing finance program bonds, serials 2025-2036, terms 2039, 2044, 2049, 2052, 2054. RBC Capital Markets.

The State of New York Mortgage Agency (Aa1///) is set to price Thursday $139.120 million of social homeowner mortgage revenue bonds, consisting of $72.765 million of non-AMT bonds, Series 258, serial 2039, terms 2044, 2049, 2054; $72.765 million of AMT bonds, Series 259, serials 2024-2036, term 2039; and $39.120 million of taxables, Series 260, serials 2024-2036, terms 2039, 2043, 2054. BofA Securities.

The Virginia College Building Authority (Aa1/AA+//) is set to price Thursday $101.900 million of University of Richmond educational facilities revenue and refunding bonds, Series 2024, serials 2027-2034, 2036, 2038-2044, terms 2049, 2054. BofA Securities.

Competitive calendar

The East Central Independent School District, Texas, (Aaa///) is set to sell $100 million of PSF-insured unlimited tax school building bonds, Series 2024, at 11:30 a.m. eastern Wednesday.

Nevada is set to sell $89.620 million of motor vehicle fuel tax highway improvement revenue bonds, Series 2024A, at 11:15 a.m. Thursday, and $45.080 million of indexed tax and subordinate motor vehicle fuel tax highway improvement revenue bonds, Series 2024B, at 11:45 a.m. Thursday.