Municipals saw a more constructive secondary trading session Thursday and mutual funds reported the third consecutive week of inflows while U.S. Treasuries improved. Stocks continued to break records after another report of hotter economic data, which is leading more participants to pare back rate cut timing expectations.

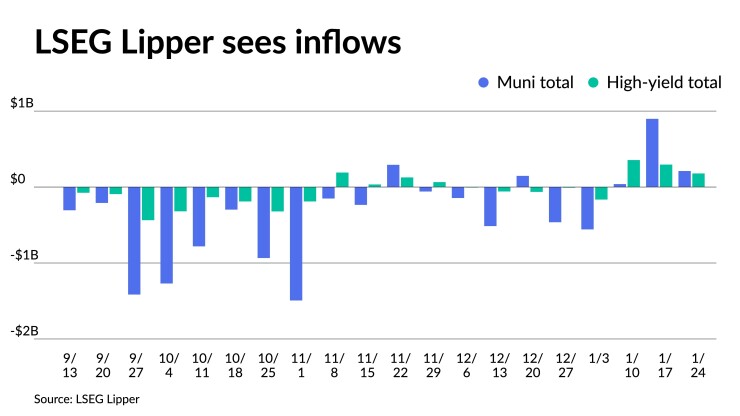

LSEG Lipper reported Thursday that investors added $210.6 million to municipal bond mutual funds for the week ending Wednesday after inflows of $898 million the week prior.

High-yield also saw inflows of $179 million after inflows of $295.3 million the week prior.

The advance look at fourth quarter gross domestic product showed a strong economy, with inflation at the Federal Reserve’s target level, leading economists to expect rates to remain higher for longer.

The report “caps a year of stellar economic growth performance,” said Olu Sonola, head of Fitch U.S. regional economics. “The Fed will likely not be in a hurry to cut rates, if the data continues to come in this hot.”

Triple-A yields saw some bumps on the short end but underperformed USTs, which improved across the curve. Ratios rose accordingly to the day’s moves.

The two-year muni-to-Treasury ratio Thursday was at 63%, the three-year at 63%, the five-year at 61%, the 10-year at 60% and the 30-year at 83%, according to Refinitiv Municipal Market Data’s 3 p.m. EST read. ICE Data Services had the two-year at 64%, the three-year at 63%, the five-year at 61%, the 10-year at 60% and the 30-year at 82% at 3:30 p.m.

When the time does come for the Fed to cut rates, “there is over $5 trillion sitting in cash/money markets and we expect money to be in motion,” noted Nisha Patel, managing director of separately managed account portfolio management at Parametric.

Triple-A muni yields remain near decade highs, Patel noted. “Tax-adjusted yields are still in the 5-6% range … equity-like returns with fixed-income risks,” she said, making municipals more appealing, particularly if the Trump tax cuts expire in 2025.

However, Patel expects price weakness in the very near-term, “which we would view as an opportunity to add exposure, as muni pricing recalibrates to more robust supply in the coming weeks/months.”

“Right now, AAA 10-year munis are at 60% (up from 56%) of USTs and we believe approximately 65% represents fair value,” she said. “In the interim, munis are susceptible to a Treasury sell-off if incoming data remains robust and the market questions its rate cut expectations.”

Bond Buyer 30-day visible supply sits at $5.65 billion and next week is expected to be lighter, as is typical during a Federal Open Market Committee meeting week.

The largest new-issues to test the market next week will be the New York State Thruway Authority (A1/A+//), which will bring $1.03 billion of general revenue bonds, and the Massachusetts Development Finance Agency (Aa2/AA//), which has $442.355 million of Children’s Hospital issue revenue bonds on the calendar Tuesday before the conclusion of the Fed meeting.

In the primary market Thursday, the last sizable deals of the week priced.

J.P. Morgan priced for the Nebraska Investment Finance Authority (/AAA//) $139.27 million of single-family housing revenue bonds.

The first tranche, $105 million of non-AMT social bonds, Series 2024A, with all bonds pricing at par — 3.25s of 9/2024, 3.45s of 3/2029, 3.45s of 9/2029, 3.75s of 3/2034, 3.8s of 9/2034, 4.1s of 9/2039, 4.5s of 9/2044, 4.7s of 9/2049 and 4.8s of 9/2054, callable 3/1/2033.

The second tranche, $34.27 million of taxables, Series 2024B, saw all bonds price at par — 4.944s of 9/2024, 4.889s of 3/2029, 4.939s of 9/2029 and 5.428s of 3/2033 — except 6.25s of 9/2049 at 5.389%, callable 3/1/2033.

In the competitive market, the Florida Department of Transportation (Aaa/AAA/AAA/) sold $190.010 million of right-of-way acquisition and bridge construction bonds, Series 2024A, with 5s of 7/2024 at 3.00%, 5s of 2029 at 2.47%, 5s of 2034 at 2.54%, 5s of 2039 at 3.15%, 4s of 2044 at 3.89%, 4s of 2049 at 4.13% and 4.125s of 2053 at 4.23%, callable 7/1/2033.

AAA scales

Refinitiv MMD’s scale was bumped up to two basis points: The one-year was at 2.99% (-2) and 2.71% (-2) in two years. The five-year was at 2.43% (-2), the 10-year at 2.46% (unch) and the 30-year at 3.61% (unch) at 3 p.m.

The ICE AAA yield curve was bumped one to two basis points: 2.97% (-1) in 2025 and 2.81% (-1) in 2026. The five-year was at 2.51% (-1), the 10-year was at 2.50% (-1) and the 30-year was at 3.61% (-1) at 3:30 p.m.

The S&P Global Market Intelligence municipal curve was little changed: The one-year was at 2.99% (-2) in 2025 and 2.77% (unch) in 2026. The five-year was at 2.45% (unch), the 10-year was at 2.47% (unch) and the 30-year yield was at 3.60% (unch), according to a 3 p.m. read.

Bloomberg BVAL was bumped up to one basis point: 2.96% (-1) in 2025 and 2.82% (-1) in 2026. The five-year at 2.48% (unch), the 10-year at 2.53% (-1) and the 30-year at 3.63% (unch) at 3:30 p.m.

Treasuries were firmer.

The two-year UST was yielding 4.312% (-6), the three-year was at 4.117% (-7), the five-year at 4.015% (-7), the 10-year at 4.126% (-5), the 20-year at 4.480% (-4) and the 30-year Treasury was yielding 4.373% (-3) at 3:45 p.m.

GDP

GDP grew 3.3% and the closely watched core personal consumption expenditures index was at an annual 2.0% pace.

“For those hunting for clues that the Federal Reserve is ready to take an ax to interest rates, will be sorely disappointed,” said Sophie Lund-Yates, lead equity analyst at Hargreaves Lansdown. “The U.S. economy has shown remarkable resilience in the face of higher interest rates and soaring inflation, with consumer spending once again being a driver of GDP growth.”

And while the economy has weather “more shocks than expected,” she said, it doesn’t mean “the storm will blow over without consequence.” While a soft-landing is possible, she noted, ”we’re miles away from knowing that for sure.”

Still the economy is a bit too strong “for the Federal Reserve to change course,” Lund-Yates said. “That could lead to some upset on the markets, which remain optimistic that cuts are on the way sooner rather than later.”

The economy grew 2.5% in 2023, noted ING Chief International Economist James Knightley, “confounding expectations at the beginning of last year that tighter monetary policy and credit conditions would potentially lead the economy to fall into recession.”

The PCE read offers “confirmation of ‘job done’ on inflation,” he added. “As such the Fed now has huge scope to cut rates. We just think they will wait a little longer to make sure they are really, really confident they can afford to cut.”

Based on estimates of the neutral rate, the Fed can cut 300 basis points “to merely return us to neutral.”

“The momentum in growth gives the Fed latitude to hold rates higher for longer,” Morgan Stanley said in a note lead authored by its Chief U.S. Economist Ellen Zentner. Morgan Stanley expects 100 basis points of cuts this year, with the first in June.

Q4 GDP supports the belief a soft landing is possible, said Ashwin Alankar, head of Global Asset Allocation at Janus Henderson Investors. “As long as the Fed does not too eagerly cut rates and inject liquidity into the system, a second wave of inflation is at bay and the Fed will have successfully normalized prices and avoided choking the economy. Tighter policy for longer is ironically what we should cheer, otherwise this second wave could hit us.”

While the Fed will hold at its upcoming meeting, Priscilla Thiagamoorthy, senior economist at BMO, said, “with the mighty consumer still fueling economic activity, we’re not expecting a pivot anytime soon and are comfortable with our July rate cut call.”

But Wells Fargo Securities Chief Economist Jay Bryson said the positive inflation news “gives the FOMC leeway to begin an easing cycle in coming months.” Wells Fargo expects a rate cut at the May 1 meeting, “although today’s inflation data will keep market hopes for a rate cut at the March 20 meeting alive.”

Bond Buyer indexes

The weekly average yield to maturity of the Bond Buyer Municipal Bond Index, which is based on 40 long-term bond prices, rose three basis points to 4.84% from 4.81% in the previous week.

The Bond Buyer’s 20-bond GO Index of 20-year general obligation yields rose four basis points to 3.43% from 3.39% from the previous week.

The 11-bond GO Index of higher-grade 11-year GOs rose four basis points to 3.33% from 3.29%.

The Bond Buyer’s Revenue Bond Index rose four basis points to 3.71% from 3.67%.

Jessica Lerner and Gary Siegel contributed to this story.