Municipals were mixed ahead of a new-issue calendar that rebounds to more than $9 billion. U.S. Treasury yields rose further Friday as the December jobs report cast doubt on whether the Fed would start cutting rates in March. Equities were up near the close.

There was already “significant upward pressure” on Treasury yields in recent sessions, so participants should “expect Fed funds futures to lower their odds of aggressive rate cuts in the first half of 2024,” said Scott Anderson, chief U.S. economist and managing director at BMO Economics.

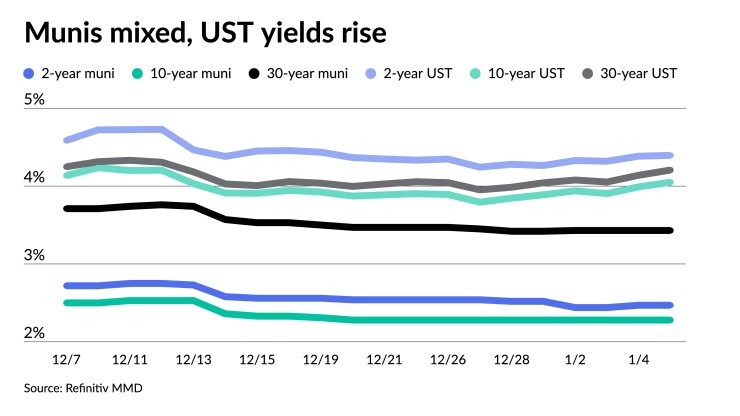

Municipals outperformed USTs Friday and throughout the week, with govies rising 14 to 18 basis points while munis were up only a few basis points, depending on the curve.

Despite the outperformance this week, and while the asset class had “a stellar December, which rounded out a very solid year, generating the best total returns for the asset class since 2019,” Barclays PLC strategists said the muni rally went “too far.”

The high-grade muni market has become “quite rich,” said Barclays strategists Mikhail Foux, Clare Pickering and Mayur Patel said in a weekly report.

This is true for the belly of the curve, around the 10-year maturity, which has been popular with separately managed accounts, they said.

“If one considers outright MMD-UST ratios, the ratio curve, or simply focuses on the 5s10s slope of the IG muni index, the 10-year portion seems very rich at the moment,” Barclays strategists said.

The two-year muni-to-Treasury ratio Friday was at 56%, the three-year at 57%, the five-year at 56%, the 10-year at 56% and the 30-year at 82%, according to Refinitiv Municipal Market Data’s 3 p.m. EST read. ICE Data Services had the two-year at 58%, the three-year at 58%, the five-year at 57%, the 10-year at 58% and the 30-year at 83% at 4 p.m.

And compared to the all-time lows in 2021, the 10-year ratio is only three to four percentage points higher, Barclays strategists noted.

The yearend rally “is particularly surprising as it ignored resilient economic data and the Fed’s messaging,” BofA strategists said.

Since the peak yield seen at the end of October 2023, the 10-year AAA muni has fallen 133 basis points, they said. This is “the same magnitude as it did from late October 2022 to early April 2023,” BofA strategists said.

Throughout the muni curve, “the retracement in tax-exempt yields will likely be quite limited, even if Treasuries’ selloff turns out to be sizeable,” said BofA strategists.

“Rich muni ratios are a negative factor, but demand/supply conditions are way too imbalanced,” they said.

Barclays strategists expect issuance to ramp up later this month.

The new-issue muni calendar rebounds to an estimated $9.058 million next week with $8.098 billion of negotiated deals on tap and $959.7 million on the competitive calendar, according to Ipreo and The Bond Buyer.

The largest deal is

Dallas leads the competitive calendar with $223.6 million of combination tax and revenue certificates of obligation, followed by $161.8 million of GO debt from The Stillwater Independent School District No. 834, Minnesota.

BofA strategists expect January issuance to be $26 billion and February to be $27 billion. Additionally, principal redemptions and coupon payments are expected to be $46 billion in January and $49 billion in February, they said.

“If there is more issuance and continued outflows, coupled with rate volatility, we might see the muni market finally come under pressure — given how fast it ran through the end of last year, there is definitely some room for a correction,” Barclays strategists said. “Nevertheless, if Treasury yields remain range-bound, munis will likely remain relatively rich for now.”

BofA strategists argued a 25 to 30 basis point selloff would be “reasonable” after a 133 basis point rally, but they “doubt the retracement will be significantly more than that.”

If investors can extend duration, Barclays strategists see more value in shorter- or longer-dated bonds, but the latter is not “overly cheap by any stretch,” they said.

“Given that mutual funds dominate long-term buying, and they lost money two years in a row, it is hard to see long-dated munis rallying much in the near term,” they added.

AAA scales

Refinitiv MMD’s scale was unchanged: The one-year was at 2.69% and 2.47% in two years. The five-year was at 2.25%, the 10-year at 2.28% and the 30-year at 3.43% at 3 p.m.

The ICE AAA yield curve was little changed: 2.73% (unch) in 2025 and 2.57% (unch) in 2026. The five-year was at 2.27% (+1), the 10-year was at 2.29% (-1) and the 30-year was at 3.42% (unch) at 4 p.m.

The S&P Global Market Intelligence municipal curve was unchanged: The one-year was at 2.68% in 2025 and 2.55% in 2026. The five-year was at 2.27%, the 10-year was at 2.30% and the 30-year yield was at 3.39%, according to a 3 p.m. read.

Bloomberg BVAL saw cuts: 2.68% (+7) in 2025 and 2.55% (+3) in 2026. The five-year at 2.26% (+3), the 10-year at 2.32% (+3) and the 30-year at 3.42% (+3) at 4 p.m.

Treasuries were weaker.

The two-year UST was yielding 4.394% (+1), the three-year was at 4.176% (+3), the five-year at 4.016% (+4), the 10-year at 4.052% (+6), the 20-year at 4.363% (+7) and the 30-year Treasury was yielding 4.209% (+7) near the close.

Jobs report

The U.S. added 216,000 jobs in December, showing job growth remained strong to close out 2023.

“The combination of low unemployment, sticky wages and ongoing job creation shows the jobs market remains tight,” said ING chief international economist James Knightley.

The December payroll report was stronger than Wall Street was expecting, but the downward revision in prior months reduces the sting a little bit,” Anderson said. “A gradual labor market cooldown remains in place.”

“However, the lingering labor market resilience and strength in average hourly earnings growth could keep the Fed on the sidelines for longer than the markets currently expect,” he said.

While Knightly noted that his firm predicted 150 basis points of rate cuts for a while for 2024, “we didn’t, and still don’t, buy into the March start point priced by markets earlier this week,” he said, believing the Fed will wait until May to act.

“All in all, the report proves that the Fed may not be in a hurry to cut rates soon, as officials kept saying after the December FOMC meeting,” said Christian Scherrmann, U.S. economist at DWS.

Olu Sonola, Fitch Ratings head of U.S. regional economics, agreed, saying the report “does not scream rate cuts; it points more in the direction of curtailing recent market expectations of rate cuts starting as early as March.”

Lindsay Rosner, head of fixed-income multi sector investing at Goldman Sachs Asset Management, had similar sentiments.

“This number does question the confidence of the market around the March cut,” she said.

Scherrmann noted uncertainty is high and he expects volatility to persist.

“All eyes will now be on next week’s [consumer price index] print, but wage growth of 4.1% year-on-year still seems inconsistent with inflation converging to the 2% target on a sustained basis,” he said. “On the other hand, if the inflation rates continue to decline, the discussion will turn to profitability, which in turn will reduce the optimistic expectations for the labor markets.”

“We’ve got three inflation prints between now and the March meeting,” Rosner said. “Every number counts.”

Primary to come

Jefferson County, Alabama, (Baa1/BBB+/BBB/) is set to price Wednesday $2.284 billion of sewer revenue refunding warrants, Series 2024, serials 2024-2044, terms 2049, 2053. Raymond James & Associates.

Massachusetts (Aa1/AA+/AA+/) is set to price Thursday $1.390 million of GOs, consisting of $850 million of new-issue bonds, Consolidated Loan of 2024, Series A, serials 2026-2028, 2034-2037, 2040-2042; and $540 million of refunding bonds, 2024 Series A, serials 2027-2044. BofA Securities.

The Southeast Alabama Gas Supply District (Aa3///) is set to price Tuesday $750.065 million of Project No. 1 gas supply revenue refunding bonds, Series 2024A. Goldman Sachs.

The Conroe Independent School District, Texas, (Aaa/AAA//) is set to price Wednesday $568.105 million of PSF-insured unlimited tax school building bonds, Series 2024, serials 2025-2049. Raymond James & Associates.

The Minnesota Agricultural and Economic Development Board (A2/A//) is set to price Wednesday $500 million of HealthPartners Obligated Group healthcare facilities revenue bonds, Series 2024. Piper Sandler.

The Lewisville Independent School District, Texas, is set to price Thursday $462.655 million of unlimited tax school building bonds, Series 2024. Piper Sandler.

The North Carolina Housing Finance Agency (Aa1/AA+//) is set to price Tuesday $300 million of social home ownership revenue bonds, consisting of $200 million of non-AMT bonds, Series 53-A, serials 2025-2035, terms 2039, 2044, 2050 and 2055; and $100 million of taxables, Series 53-B, serials 2025-2035, terms 2039, 2044, 2050, 2055. Wells Fargo Bank.

The Judson Independent School District, Texas, (Aaa///) is set to price Tuesday $255 million of PSF-insured unlimited tax school building bonds, Series 2024, serials 2025-2044, terms 2049, 2053. Estrada Hinojosa & Co.

The Community College District No. 508, Illinois, (/AA/A+/) is set to price Wednesday $190.500 million of BAM-insured dedicated revenues unlimited tax general obligation refunding bonds, Series 2024, serials 2026-2043. Loop Capital Markets.

New Braunfels, Texas, (Aa1///) is set to price Thursday $148.970 million of utility system revenue and refunding bonds, Series 2024, serials 2024-2055. HilltopSecurities.

Competitive

The Stillwater Independent School District No. 834, Minnesota, is set to sell $161.830 million of GO school building, facilities maintenance and refunding bonds, Series 2024A, at 10:30 a.m. eastern Tuesday.

Dallas is set to sell $223.620 million of combination tax and revenue certificates of obligation, Series 2024A, at 11 a.m. Thursday.