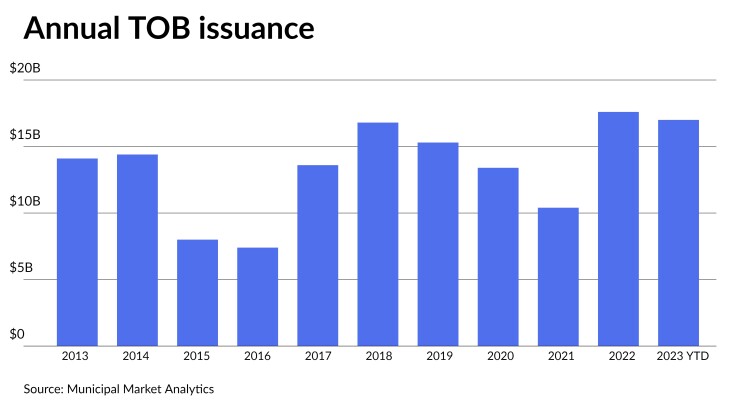

Tender option bond volume is growing and is expected to reach a 10-year high this year, according to Municipal Market Analytics.

About $17 billion of TOBs have been issued so far in 2023, which is on pace to eclipse last year’s $17.6 billion, MMA said. The outstanding TOB market is at about $50 billion from highs of nearly $500 billion prior to the Financial Crisis of 2008.

“The product’s strong issuance but constrained outstanding amount reflects the economics and management of previous TOB trades and adaptation to current market conditions,” said MMA Managing Director Lisa Washburn in the firm’s weekly Outlook report. “Rising rates since the near-zero interest rate environment during the pandemic period led to the collapse or unwind of nearly three-quarters of TOB trades put on during that time.” Many TOBs now are being issued as a replacement.

While the growth of TOBs might lead investors and regulators to grow concerned over related market risks, “recalling the outsize harm these products caused during the Financial Crisis,” MMA notes that 2023 “seems likely to be different.”

Washburn noted the current smaller size of the outstanding TOB market also reflects a reduced credit concentration risk with less exposure to insured bonds — many of which in that time were covered by the failed insurers — among programs, and lower overall leverage.

Washburn said issuer-driven TOBs are also increasing. “Issuers looking to wait out current market conditions for a better rate environment and/or improved sector operating conditions (e.g. hospitals) may opt to issue floating rate notes as a private placement, funded by a TOB issuance,” she said. “This strategy allows the issuer to gain access to capital at a variable rate that typically can be converted to fixed when conditions improve and can reduce issuance costs because of lower disclosure requirements.”

Bonds used for new trusts created by funds seeking leverage “are heavily weighted towards sectors that have higher coupons and/or provide extra spread in the high-grade arena,” Washburn noted. About 40% of TOBs created in 2023 year to date used hospital or housing bonds, she said.

Despite the changes this year, the product still “can add incremental risk to the market during periods of disruption, noting in particular March 2020 when unwinds rose, increasing bond selling just as mutual funds sought to raise cash to address outflows and spiking short-term rates,” Washburn added.

To create TOB trusts, an investment fund or a bank deposits high-quality long-term bonds into the trusts. The trust issues two securities: one called a “floater” and one called an “inverse floater.” The “floater” security will be sold to money market funds and other institutional short-term investors. The security’s purchasers can call it at any time and it carries low short-term interest rates.

The “inverse floater” is held by the funds or banks starting the process. Through it, the funds or banks get the interest from the long-term bonds minus payments to the floater holders and some administrative charges.

If the floaters are tax-exempt, they provide the muni market with a flexible form of investment. Since leverage is involved in the TOB trusts, they can provide banks and funds higher interest returns on their tax-exempt bonds.

“The TOBs that are being issued in replacement [in the last two or three years] are less levered, with the average leverage/gearing for trusts issued in 2022-23 at approximately 4:1 compared with the 6:1 during 2020-21,” Washburn said. The current leverage of aggregate outstanding TOBs sits closer to 4:1, she said.

Additionally, since rates began rising in earnest in 2022, banks have been shifting to tax-exempt tender option bond programs from taxable TOBs.

When interest rates were at near or record lows, bank-sponsored tax-exempt TOBs were less than 5% of the market by dollar volume in 2020 and were about 8% in 2021, according to Standard & Poor’s Financial Services data. However, the portions increased to about 35% in 2022 and to about 87% this year through Sept. 18.

Bank-sponsored trusts that issue TOBs experience short-term interest rates as a cost.

During the ultra low-rate environment in the COVID-19 period from May 2020 to April 2022, with the costs identical between the tax-exempt and taxable varieties, banks turned to the greater returns of the taxable instruments.

“As interest rates began to rise in 2022, however, tax-exempt financing once again became an attractive alternative for banks,” said S&P Global Ratings Associate Director Joshua Saunders in a Sept. 19 report.

Over the last four or five months, the Securities Industry and Financial Markets Association (SIFMA) Municipal Swap Index, a measure of short tax-exempt rates, has gyrated from 2.2% to 4.19%. By comparison, in the same period the Secured Overnight Financing Rate (SOFR), a measure of taxable rates based on U.S. Treasury bond trading, has climbed to about 5.3%.

“Although interest rates alone do not necessarily explain the recent shift to tax-exempt financing [in TOBs], they represent a significant driver,” Saunders said.

When interest rates were near zero for both taxable and tax-exempt short-term borrowing, it was less complicated for TOBs to offer taxable offerings, said Mary Jo Ochson, chief investment officer for tax-free liquidity investment area and short-term municipal bonds at Federated Hermes. With the taxable issuance, there are fewer legal hurdles to get over than with tax-exempts. These advantages led TOBs to offer taxable floaters in that period.

Washburn said the last two years were a return to the earlier, pre-COVID patterns for bank-sponsored TOBs, where roughly 80% to 95% of them were tax-exempt.

However, according to S&P data about 62% of bank-sponsored TOBs by dollar volume were tax-exempt in 2018 and about 41% of them were tax-exempt in 2019.

Bank-sponsored TOBs amount to about 30% of all TOBs, with the remainder being sponsored by investment funds, Washburn said.

In the first half of this year, JPMorgan (33.6%), Barclays (19.7%), and BofA Securities (11.9%) sponsored the most TOBs, by dollar volume, according to S&P.