Municipal triple-A yield curves were little changed Wednesday as the primary market demanded investor attention and were well received. U.S. Treasuries were weaker, and equities ended mixed.

Several large new-issues priced led by $1.018 billion of the University of Chicago revenue bonds from the Illinois Finance Authority (Aa2/AA-/AA+/), with yields bumped seven to 15 basis points from Tuesday’s retail pricing, along with the Triborough Bridge and Tunnel Authority’s $600 million of climate-certificate payroll mobility tax senior lien green bonds.

Illinois’ tax-exempt GOs repriced yesterday afternoon with bumps of 10 to 13 basis points.

After nine credit upgrades, Illinois received “tremendous feedback from the bond market … and especially from retail investors, who came in at approximately $1.5 billion in orders given the stronger ratings,” Paul Chatalas, director of capital markets for Illinois, said in a statement. ”Based on this very strong demand, the state accelerated its pricing to capture positive momentum and received more than $12 billion in overall orders from 150 accounts. The final result showed some of the tightest credit spreads the state has received in recent history and a notably expanded base of investors who have shown that the state’s tremendous fiscal progress are already paying off for the citizens of Illinois.”

May will be a macro-dependent month for fixed income, said Nisha Patel, managing director of separately managed account portfolio management at Parametric.

The upcoming data points this month will create some volatility and possibly fluctuations in UST yields, she said.

Currently, there is “large demand” on the front end of USTs, with the three-month and six-month auctions “very strong even in the face of record offering size, said Bryon Anderson, head of Fixed Income at Laffer Tengler Investments.

While UST yields rose Wednesday, they have still fallen from the highs seen on April 30.

Since then, the two-year UST has fallen from a six-month high of 5.04% to 4.842% and the 10-year from 4.687% to 4.495%.

“We have a tale of two markets right now, with yields increasing when we get elevated inflation data and decreasing when we have increasing unemployment or slowing job growth,” Anderson said.

The Fed is slowing its balance sheet runoff to $25 billion, down from $60 billion a month prior, “which should cause a firming of the Treasury market short term,” he said.

“Ultimately, we are in an increasing yield trend with inflation data as the priority but with consumers showing recent weakness, we are cautious,” according to Anderson.

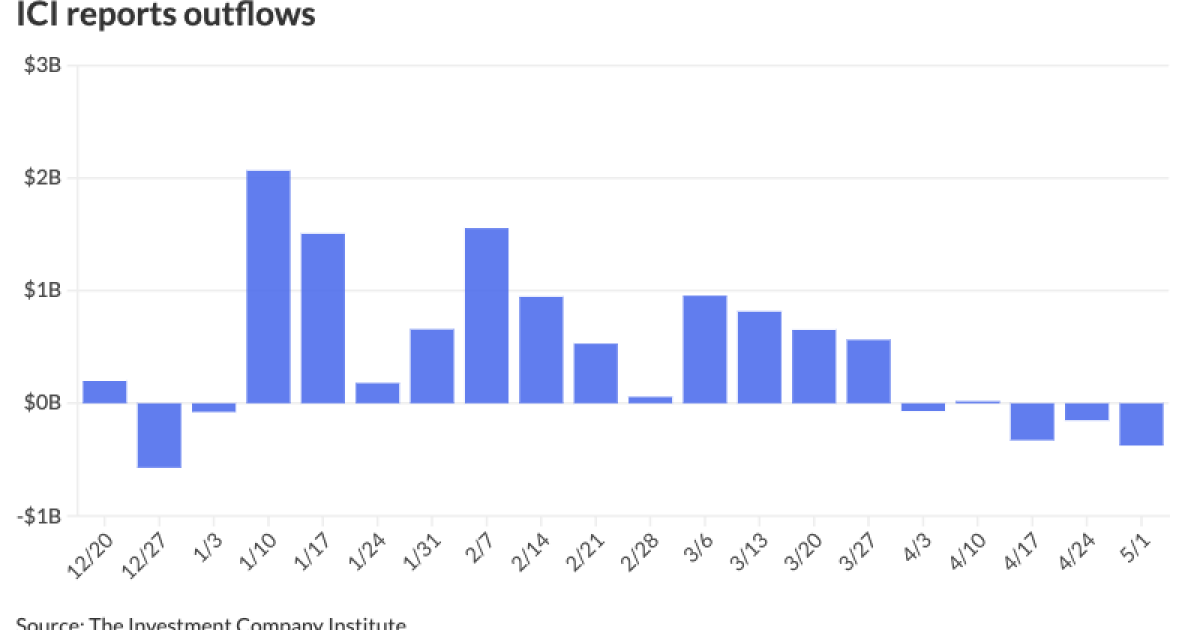

The Investment Company Institute reported outflows from municipal bond mutual funds for the week ending May 1, with investors pulling $375 million from funds following $151 million of outflows the week prior. This differs from LSEG Lipper, which reported

ICI reported exchange-traded funds saw inflows of $319 million following $776 million of inflows the week prior.

Despite recent outflows, there have been inflows year-to-date of $9.5 billion, according to ICI.

“We can go a lot more in the direction of inflows if the narrative changes from a Fed cut standpoint,” Patel said.

If there were more data to “support” the Fed’s decision to cut rates sooner than the market expects, that could start “stemming” flows from the sidelines into fixed income, she said, especially during this reinvestment period over the coming few months.

There are heavy reinvestment flows in the summer months of June through August.

This, she said, supports an environment for muni-UST ratios to stay “fairly compressed” at these levels.

The two-year muni-to-Treasury ratio Wednesday was at 63%, the three-year at 63%, the five-year at 60%, the 10-year at 60% and the 30-year at 81%, according to Refinitiv Municipal Market Data’s 3 p.m. EST read. ICE Data Services had the two-year at 63%, the three-year at 62%, the five-year at 61%, the 10-year at 61% and the 30-year at 81% at 3:30 p.m.

“You have the strength of demand coming in that could be substantially higher than the amount of issuance,” she said. “So it’s hard to see an environment outside of a complete breakout of Treasury yields to where muni yields could get so soft.”

In the primary market Wednesday, RBC Capital Markets priced for institutions $1.018 billion of the University of Chicago revenue bonds from the Illinois Finance Authority (Aa2/AA-/AA+/), with yields bumped seven to 15 basis points from Tuesday’s retail pricing: The first tranche, $633.89 million of Series 2024A, saw 5s of 4/2031 at 2.97% (-10), 5s of 2034 at 3.00% (-10), 5s of 2040 at 3.49% (-13), 5.25s of 4/2044 at 3.75% (-13), 5.25s of 2049 at 4.01% (-9) and 4.25s of 2052 at 4.34% (-7), callable 4/1/2034.

The second tranche, $384.38 million of Series 2024B, saw 5s of 4/2027 at 3.15% (-10), 5s of 2029 at 3.00% (-10), 5s of 2034 at 3.00% (-10) and 5.25s of 4/2039 at 3.39% (-15), callable 4/1/2034.

BofA Securities priced for the Triborough Bridge and Tunnel Authority (/AA+/AA+/AA+/) $600 million of climate-certificate payroll mobility tax senior lien green bonds, Series 2024B. The first tranche, $387.995 million of Series 2024B-1, saw 5s of 5/2045 at 3.74%, 5s of 2046 at 3.81%, 5.25s of 2054 at 4.02% and 4.125s of 2054 at 4.21%, callable 5/15/2034.

The second tranche, $100 million of Series 2024B-2, saw 5s of 5/2031 at 2.85%, callable 2/15/2031.

The third tranche, $112.69 million of Series 2024B-3, saw 5s of 11/2043 with a mandatory tender date of 11/15/2025 at 3.36%, noncall.

Jefferies priced for the

The second tranche, $204.27 million of refunding bonds, Series 2024B, saw 5s of 7/2025 at 3.19%, 5s of 2029 at 2.73%, 5s of 2034 at 2.80%, 5s of 2040 at 3.29%, 5s of 2044 at 3.59% and 5s of 2045 at 3.62%, callable 1/1/2034.

Wells Fargo priced for Energy Northwest (Aa1/AA-/AA/) $266.8 million of electric station revenue bonds. The first tranche, $189.77 million of Project 1 refunding bonds, Series 2024-B, saw 5s of 7/2025 at 3.31% and 5s of 2027 at 3.02%, noncall.

The second tranche, $10.13 million of Columbia Generating Station bonds, Series 2024-B, saw 5s of 7/2032 at 2.83%, noncall.

The third tranche, $66.9 million of Project 3 refunding bonds, Series 2024-B, saw 5s of 2028 at 2.90%, noncall.

J.P. Morgan priced for Polk County, Iowa, (Aaa/AAA//) $112.35 million of exempt facility bonds – AMT GO capital loan notes, Series 2024A, with 5s of 6/2026 at 3.58%, 5s of 2029 at 3.31%, 5s of 2034 at 3.33%, 5s of 2039 at 3.71% and 5s of 2044 at 4.02%, callable 6/1/2032.

J.P. Morgan priced for the Kentucky Asset/Liability Commission (/AA//) $107.44 million of Federal Highway Trust Fund first refunding project notes, 2024 Series A, with 5s of 9/2024 at 3.62% and 5s of 2026 at 3.18%, noncall.

In the competitive market, Hempstead, New York, (Aaa///) sold $194.547 million of public improvement serial bonds, to Jefferies, with 5s of 5/2025 at 3.05%, 5s of 2029 at 2.52%, 4s of 2034 at 2.70%, 4s of 2039 at 3.25%, 4s of 2044 at 3.80% and 4s of 2047 at par, callable 5/1/2032.

AAA scales

Refinitiv MMD’s scale was unchanged: The one-year was at 3.25% and 3.07% in two years. The five-year was at 2.72%, the 10-year at 2.69% and the 30-year at 3.77% at 3 p.m.

The ICE AAA yield curve was bumped up to three basis points: 3.23% (-3) in 2025 and 3.08% (-2) in 2026. The five-year was at 2.72% (flat), the 10-year was at 2.70% (-1) and the 30-year was at 3.74% (-1) at 3:30 p.m.

The S&P Global Market Intelligence municipal curve was unchanged: The one-year was at 3.29% in 2025 and 3.06% in 2026. The five-year was at 2.69%, the 10-year was at 2.68% and the 30-year yield was at 3.76%, according to a 3 p.m. read.

Bloomberg BVAL was unchanged: 3.31% in 2025 and 3.11% in 2026. The five-year at 2.66%, the 10-year at 2.64% and the 30-year at 3.79% at 3:30 p.m.

Treasuries were weaker.

The two-year UST was yielding 4.842% (+1), the three-year was at 4.657% (+2), the five-year at 4.502% (+3), the 10-year at 4.495% (+3), the 20-year at 4.737% (+3) and the 30-year at 4.639% (+3) at 3:30 p.m.

Primary to come:

Columbus, Ohio, (Aaa/AAA/AAA/) is set to price Thursday $467.455 million of various purpose GOs, consisting of $293.755 million of unlimited tax bonds, Series 2024A; $22.29 million of limited tax bonds, Series 2024B; $76.72 million of taxable unlimited tax bonds, Series 2024C; $15.385 million of taxable limited tax bonds, Series 2024D; and $59.305 million of unlimited tax refunding bonds, Series 2024-1. J.P. Morgan.

San Francisco (Aaa/AAA/AAA/) is set to price Thursday $345 million of GO refunding bonds, Series 2024-R1, serials 2025-2036. Stifel.

The New Jersey Health Care Facilities Financing Authority (A1/AA-//) is set to price Thursday $256.055 million of RWJ Barnabas Health refunding bonds, Series 2024B. Jefferies.

The Racine Unified School District, Wisconsin, is set to price Thursday $150 million of GO promissory notes, Series 2024. Baird.

The Utah Housing Corp. (Aa2///) is set to price Thursday $114.805 million of taxable single family mortgage bonds, 2024 Series F. Jefferies.