Municipals were little changed Wednesday, while U.S. Treasury yields fell slightly and equities ended the session down after the Federal Open Market Committee’s December meeting minutes offered little insights into future rate cuts.

The two-year muni-to-Treasury ratio Wednesday was at 56%, the three-year at 58%, the five-year at 58%, the 10-year at 58% and the 30-year at 85%, according to Refinitiv Municipal Market Data’s 3 p.m. EST read. ICE Data Services had the two-year at 59%, the three-year at 58%, the five-year at 57%, the 10-year at 59% and the 30-year at 84% at 3:15 p.m.

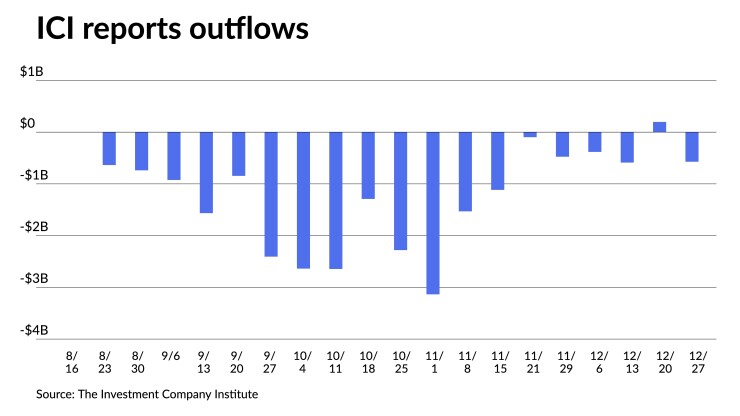

The Investment Company Institute Wednesday reported inflows into municipal bond mutual funds for the final week of 2023 ending Dec. 27, with investors adding $572 million to the funds following $198 million of inflows the week prior. Exchange-traded funds also saw inflows of $341 million following $982 million of inflows the week prior.

While the final two weeks of 2023 ended slowly for munis, that does not mean 2024 will start the same, said Matt Fabian, a partner at Municipal Market Analytics.

“Rather, this year has favorable potential for 1Q activity, noting an unusually large scheduled reinvestment potential in January and February,” including $19 billion of maturities plus calls in January and $24.9 billion in February, he said.

Market sentiment is different this year than it was going into 2023, said Tom Kozlik, managing director and head of public policy and municipal strategy at HilltopSecurities.

On both issuer and investor sides, there will be much sentiment discovery happening this week and next, he said.

Many market participants, Kozlik said, will be reading an “extra amount into what comes out from related to the Fed over the next week or two because folks are trying to figure out what that next level of direction is going to be in the market.”

“In typical fashion after the holidays, the market is slowly starting to come back to normal, with investors evaluating their portfolios for the new year,” according to Roberto Roffo, managing director and portfolio manager at SWBC.

Most are expecting the Federal Reserve to start lowering interest rates due to a slowing economy, Roffo said Wednesday.

He suggested that could alter buying habits among individuals.

“I believe that investors will use any substantial weakness to add duration and yield,” Roffo said.

There is not currently much primary market issuance, which Kozlik noted could be a good thing for market participants who want to get things done.

There will be a lot of reinvestment money coming into the market over the next several weeks, according to Kozlik, leading to the supply-demand dynamic being at the forefront of market participants’ minds this year, he said.

“Folks are wondering if institutional demand going to come back and when it will come back,” he said.

Seasonal expectations typically are for lower issuance in January, “but the 4Q drop in yields, very reasonable concern among bankers and borrowers about rate volatility in the near term, and an overhang of callable targets left over from last year build potential energy for a surge in tax-exempt refundings and tenders, at a minimum,” Fabian said.

He expects this will eventually “be supplemented with a moderate uptick in new-money financings, although this is more about credit fundamentals,” such as sustained financial health and the implementation of delayed/stuttered 2023 borrowing plans, than market fundamentals, including better demand.

“The latter is substantially less predictable, depending primarily on a resumption of 2023 [separately managed account and exchange-traded fund] buying, secondarily on a (reasonable but unreliable) return of mutual fund inflows, and not at all on renewed interest from banks and insurance companies,” Fabian said.

Banks are likely to remain net sellers throughout the year “despite the movement of rates and prices: this may undermine relative value and nominal price performance but also preserve something of current investor income opportunities a bit longer,” according to Fabian.

“And macro conviction should remain low, guarded by undue uncertainties that present as soon as next week when Congress begins to face meaningful political challenges in crafting a budget,” he said.

Secondary trading

Connecticut 5s of 2025 at 2.81% versus 2.81% Tuesday and 2.71% original on 12/20. DC 5s of 2025 at 2.62%-2.60%. Washington 4s of 2026 at 2.54%-2.55% versus 2.48% on 12/20.

NYC TFA 5s of 2027 at 2.38%. Hillsborough County, Florida, 5s of 2028 at 2.34% versus 2.38% Tuesday and 2.39% on 12/20. NYC 5s of 2029 at 2.36%-2.34%.

DASNY 5s of 2032 at 2.45%-2.41%. Ohio 5s of 2034 at 2.43%-2.42%. NYC 5s of 2035 at 2.53%.

Garland ISD, Texas, 5s of 2048 at 3.53%-3.52% versus 3.50% Friday and 3.54%-3.53% on 12/27. Northwest ISD, Texas, 5s of 2049 at 3.62%-3.60% versus 3.56%-3.55% Thursday and 3.58%-3.56% on 12/27.

AAA scales

Refinitiv MMD’s scale was unchanged: The one-year was at 2.65% and 2.44% in two years. The five-year was at 2.25%, the 10-year at 2.28% and the 30-year at 3.43% at 3 p.m.

The ICE AAA yield curve was slightly weaker in spots: 2.71% (-2) in 2025 and 2.55% (+1) in 2026. The five-year was at 2.25% (+2), the 10-year was at 2.30% (+1) and the 30-year was at 3.42% (unch) at 3:15 p.m.

The S&P Global Market Intelligence municipal curve was unchanged: The one-year was at 2.66% in 2025 and 2.53% in 2026. The five-year was at 2.27%, the 10-year was at 2.30% and the 30-year yield was at 3.39%, according to a 3 p.m. read.

Bloomberg BVAL was cut up to a basis points: 2.59% (unch) in 2025 and 2.50% (unch) in 2026. The five-year at 2.21% (unch), the 10-year at 2.27% (+1) and the 30-year at 3.37% (+1) at 3:15 p.m.

Treasuries were slightly firmer.

The two-year UST was yielding 4.319% (-1), the three-year was at 4.074% (-3), the five-year at 3.892% (-4), the 10-year at 3.904% (-4), the 20-year at 4.207% (-3) and the 30-year Treasury was yielding 4.052% (-3) at 3:15 p.m.

No hints on rate cuts in FOMC minutes

The minutes from the December Federal Open Market Committee meeting offered no clues as to when rate cuts would begin, and while acknowledging inflation data was more favorable, participants remained highly attentive to inflation risks.

Officials, while maintaining they will be data-dependent, “reaffirmed that it would be appropriate for policy to remain at a restrictive stance for some time until inflation was clearly moving down sustainably toward the Committee’s objective.”

When discussing “inflation, all participants observed that clear progress had been made in 2023 toward the Committee’s 2% inflation objective,” the minutes noted. “Participants observed that inflation remained above the Committee’s objective and that they would need to see more evidence that inflation pressures were abating to become confident in a sustained return of inflation to 2%.”

The economic outlook offered “a high degree of uncertainty,” officials said. With households’ balance sheets remaining strong, “the momentum of economic activity may be stronger than currently assessed,” according to participants.

After tightening during the summer months, financial conditions eased between meetings, the minutes said. “Many participants remarked that an easing in financial conditions beyond what is appropriate could make it more difficult for the Committee to reach its inflation goal.”

Other upside risks to inflation that officials cited were “geopolitical developments, a potential rebound in core goods prices following the period of supply chain improvements, or the effects of nearshoring and onshoring activities on labor demand and inflation.”

Downside risks included a larger-than-expected impact from previous policy tightening, weaker household balance sheets, the negative effect of lower foreign growth, “and lingering risks of further tightening in bank credit.”

They also see “an unusually elevated degree of uncertainty” and the possibility “the economy could evolve in a manner that would make further increases in the target range appropriate.” Some members said circumstances could dictate holding rates for longer than currently anticipated.

Gary Siegel and Christine Albano contributed to this story.